In the last few weeks, the wage type management in KLARA has been adjusted in line with the specifications of SECO (State Secretariat for Economic Affairs). The calculations in KLARA are based on these specifications. Further information and help in making calculations can be found at the SECO website in the forms area.

You can enter any short-time work simply in your pay slips in KLARA. You must proceed as follows for this:

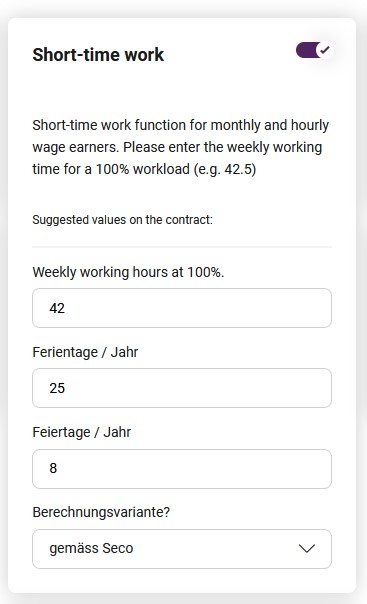

Under Company – Salary functions activate the tile Short-time work. Then click on this tile and enter the contractually agreed weekly working hours for your company as well as the holiday days and public holidays. Please note that the general weekly working hours for full-time employees are entered here. The data entered here serves merely as a basis for calculation for the new salary types for short-time work.

In addition, you have the option of selecting an alternative calculation method “Simplified method”. If this option is not explicitly chosen, the SECO option is used as default in the calculation.

Why is there a further calculation option? There are various recommendations as to how the pay slips for shorttime work should be set out. For this reason, we have also made the highly simplified version available. This type of calculation only applies for monthly wage earners. In the case of hourly rate workers, the SECO option continues to be used, since this deals with the problem of supplements in a straightforward manner.

Just as with the agreed salary, it is not allowed to change this information during the period of short-time work for this calculation type either!

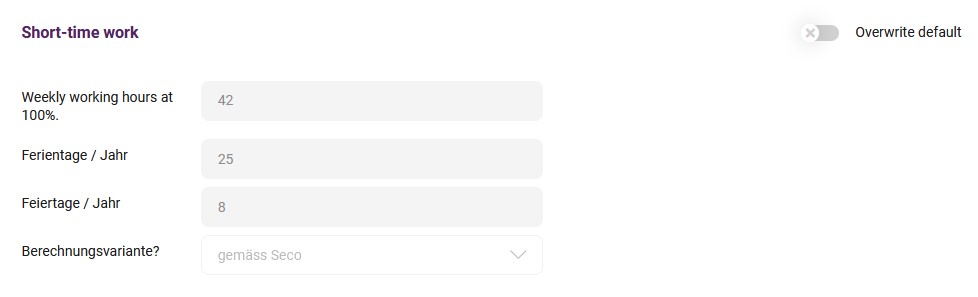

If you should have agreed different data in the employment contract for some of your employees, this can be overridden in the employee management for each employee on an individual basis. For this go to “Employee – Manage employees – Change employment (in the quick menu)”.

If you have employees with deviations, e.g. with different weekly working hours or fewer holiday days than standard in the company, these can be adjusted here.

Employees working on a part-time basis do not need to be overridden individually here. This is taken into account automatically in the calculation.

Now the newly generated salary type can be filed in the corresponding pay slip. Click in the pay slip on “Add salary components” and search accordingly for the required salary type:

- Reduction Short-time work lost hours (monthly wage earner)

- Short-time work lost hours (hourly wage earner)

- Lost hours short-term work / bad weather compensation

If you have selected the correct salary type for the employee according to your needs, you can start with the entry.

Monthly wage earners

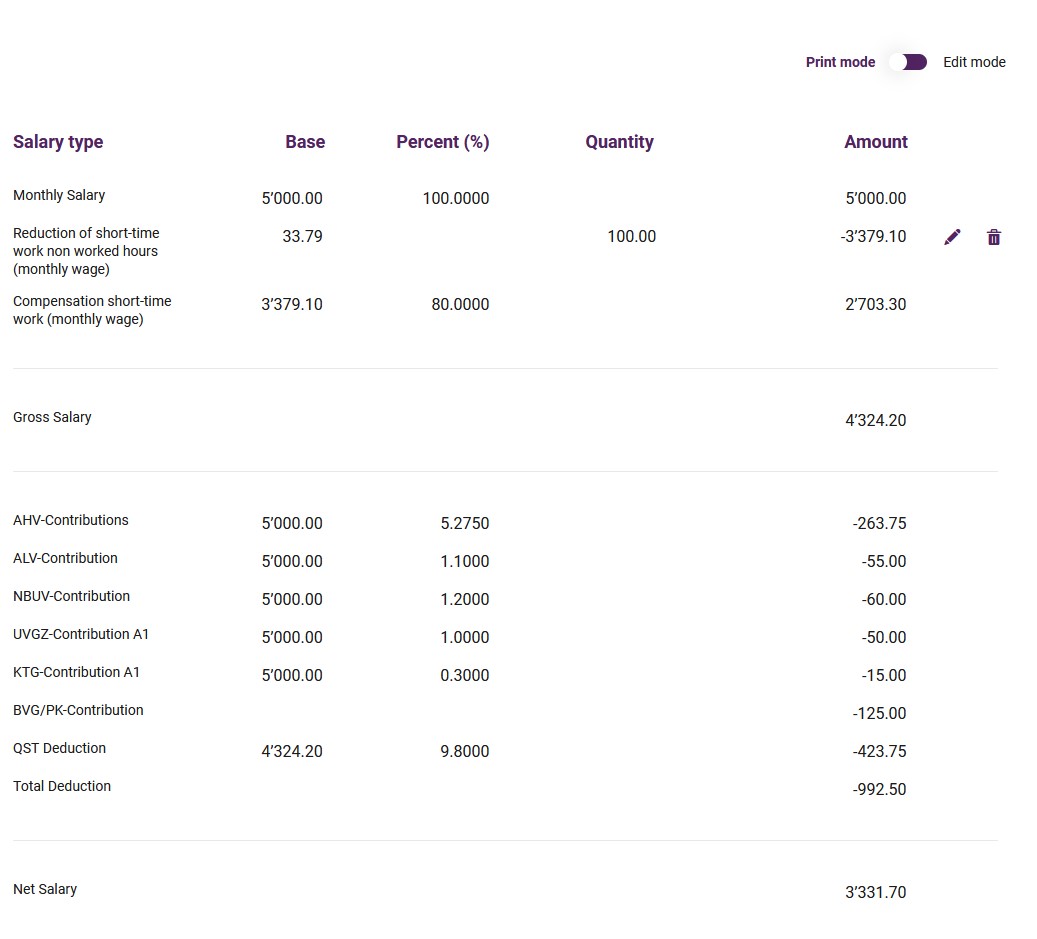

In the example for the monthly wage earner entry, it was not possible for 100 hours to be worked in the current salary period. KLARA now calculates the new gross salary based on the stated lost hours.

Calculation in the case of monthly wage earners

These employees do not have any deviating information in their contracts with regard to “Short-time working”, thus the company information applies

- 42 weekly hours of work

- 25 holiday days

- 8 public holidays

The calculation for the creditable hourly service is thus as follows:

- Working days 262

- Less 25 holiday days

- Less 8 public holidays

Total 229 net working days

The contractually agreed weekly working hours are 42 (8.4 per day)

229 x 8.4 = 1923.6 net working hours per year / 12 gives 160.3 per month

The monthly salary is assumed on the basis of 100% and if the 13th month salary is active, then 1/12 is extrapolated:

For us 5000.-- + 13th month salary = 416.66 = 5416.66 / 160.3 = 33.79

With this calculated hourly rate, the lost hours are deducted and 80% of the same credited once again.

The social insurance bases are taken into account in this to 100%.

Calculation of the monthly wage earners in the case of the “simplified calculation”:

In this simplified calculation it is assumed that holidays, public holidays and the 13th month salary are calculated at 100%. The ALV (unemployment insurance) payments to the employer include these shares.

Thus, only the current values (without offsetting) are calculated here.

The weekly hours (on a 100% basis) are multiplied by 52 weeks and divided by 12 months:

Example: 42 x 52 / 12 = 182 average hours per month

The current monthly salary is divided by these 182 hours which gives the hourly rate for the lost hours. 80% of these are compensated.

The social insurance bases are also taken into account here to 100%.

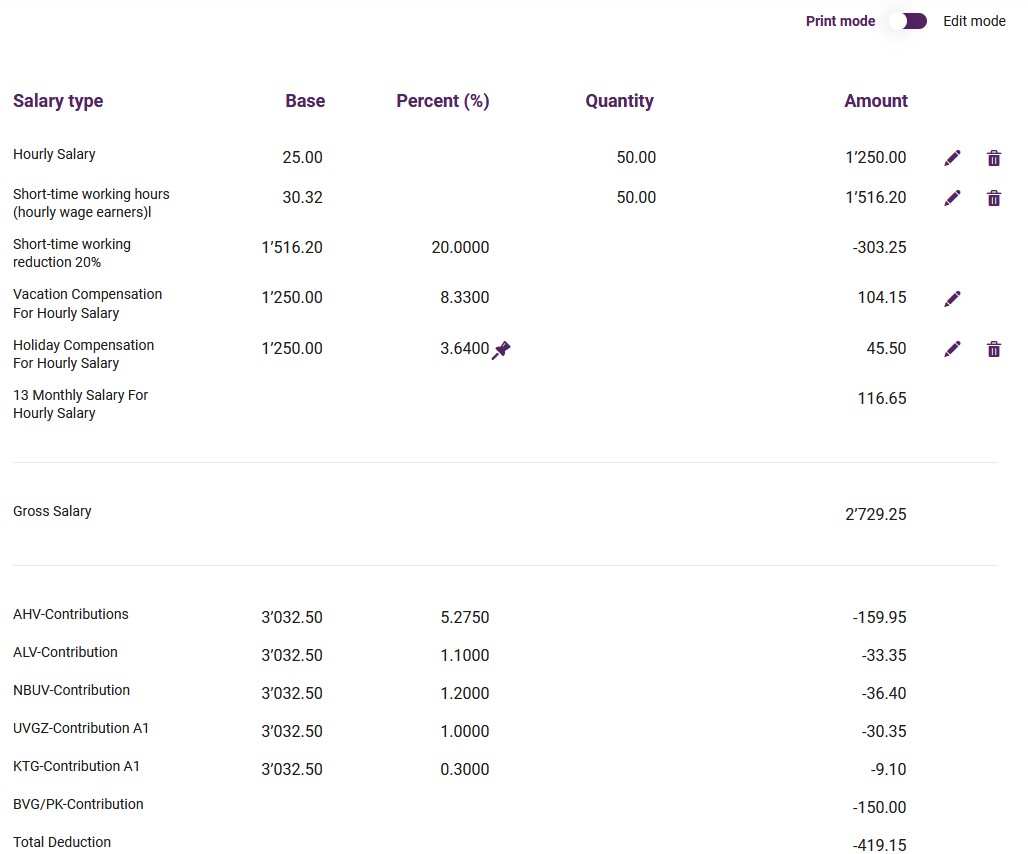

Calculation for hourly wage earners

The creditable hourly earnings according to SECO are calculated as follows:

Normal hourly salary 25.00

Offset hourly salary 27.08 if the 13th month salary is active = 8.33%

Offset hourly salary 30.32 with pro rata holiday days and public holidays

4 weeks holiday and 8 public holidays = 11.97%

The days of the year are for the year 2020 = 262

262 days minus 20 holiday days minus 8 public holiday days gives 234 net working days.

28 days / 234 days gives a % rate of 11.97%

Thus, the lost hours in our example are calculated at the hourly rate of 30.32 – 100% as payment and 20% as deduction.

Since the supplements have all been taken into account here, the lost hours are no longer taken into account in the standard supplements (holiday share, public holidays and 13th month salary).

The 100% payment of the lost hours is fully taken into account in the social insurance bases.

Salary type “Loss of wages short-time work / bad weather compensation”

With the aforementioned short-time work option, only the monthly/hourly salary and any local allowance are taken into account in the calculation. We therefore assume that the local allowance is declared under “Other salary components” in the short-time work. This means that the salary component “Local allowance” is included in the calculation of the creditable hourly rate.

If you should have included further specialities, it is possible that this calculation is not correct for you. In this case you have the option of calculating the corresponding amounts manually and of recording the amounts calculated

with the following salary types:

Loss of earnings short-time work / bad weather compensation (hourly wage earners) -> Lost hours at 100% including pro rata holiday days, public holidays and 13th month salary

ALV compensation -> 80% of the lost hours 100%

Salary deduction short-time work / bad weather compensation (monthly wage earners) -> Deduction to 100% of the lost hours

ALV compensation -> compensation 80% of the lost hours

Correct posting in KLARA accounting

In KLARA the salaries are automatically posted after each pay slip. How are the indemnification payments posted upon receipt?

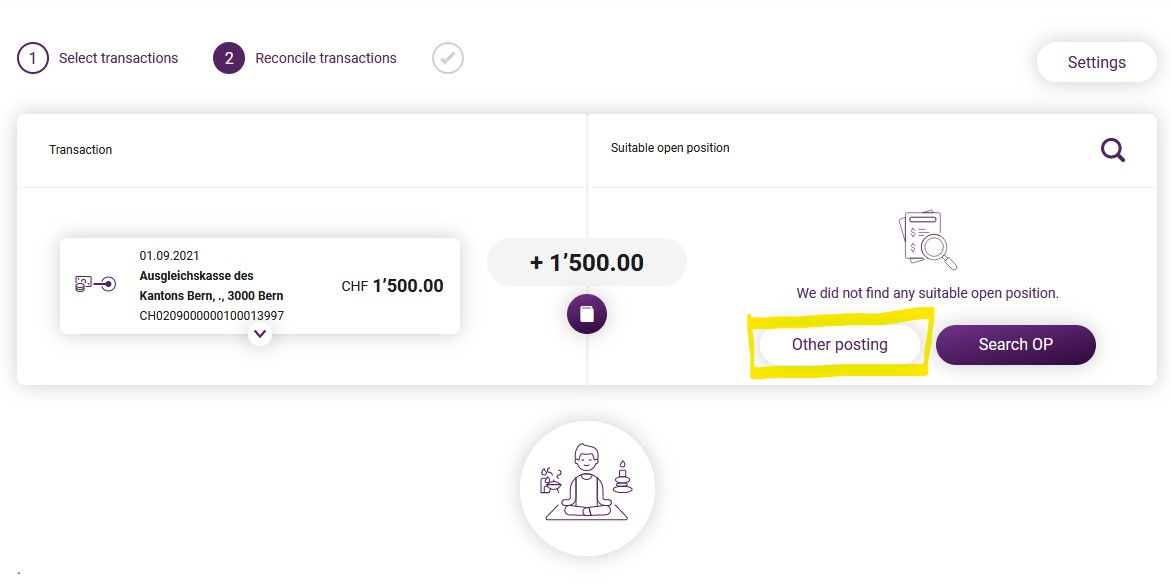

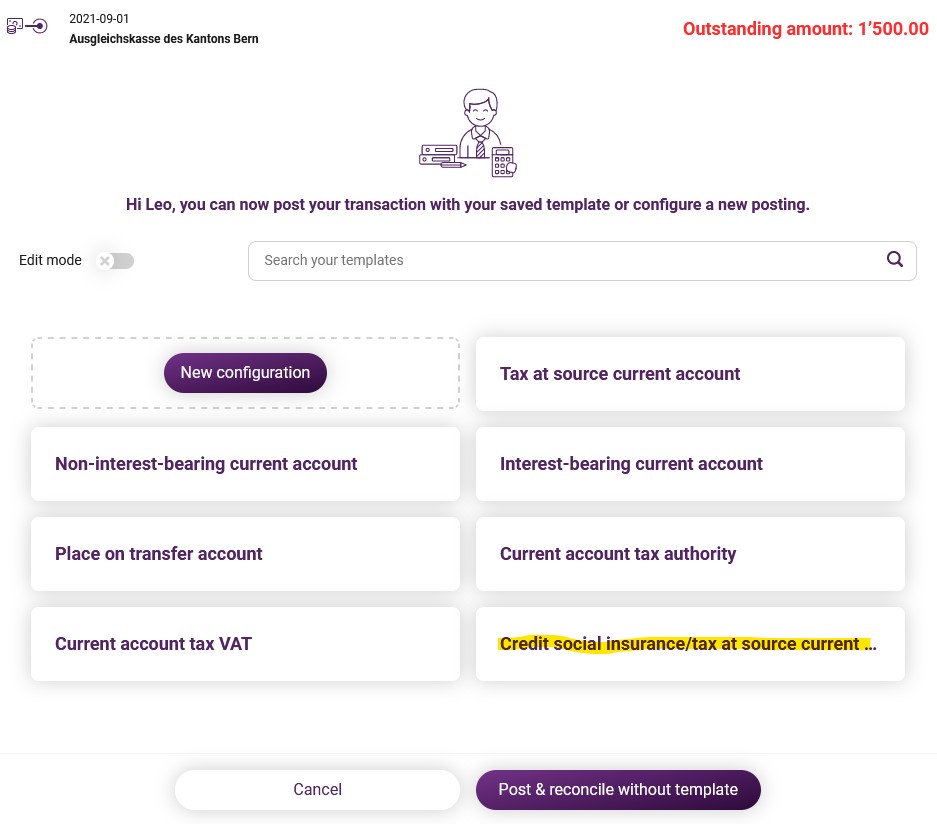

Posting the indemnification payments via bank reconciliation

As soon as the indemnification payment has reached your bank account, you can post it in KLARA via the bank reconciliation. Click on the button “Other posting” next to the payment you have received and then select there “Current account social insurance / withholding tax”. Now you can select the corresponding social insurance in order to conclude the posting.

Thus, the indemnification is automatically posted using the debit placement method.

Salary postings prior to 24.04.2020

If a salary run with short-term work compensation is carried out before 24.04.2020, we recommend carrying out the following additional posting.

Via the function “Manual posting” you can make a posting in the “General ledger”. Select the account “2270 Current account social insurances / withholding tax authorities”, the type “Current account social insurances” and select the social insurance concerned. In the debit side add the share of the employee compensation for the short-time work and select a tag, e.g. “Short-time work”. For the offsetting account select the account “5000 Wage expenses”, select the appropriate tag for you, e.g. “Social insurance benefit” and enter the same amount in the credit side.

For the posting of salaries from 24.04.2020 this manual posting is no longer necessary.

VAT

Short-time working compensation is not subject to VAT. According to the Swiss Federal Tax Administration, short-time working compensation must be declared in the VAT statement under “Other cash flows, point 910”.