The revision of the withholding tax on earned income serves to standardise the calculation of withholding tax between the cantons. The basis for this is the FTA's Circular No. 45, which specifies the Federal Act on the Revision of Withholding Tax and contains numerous calculation and application examples. This article is a summary of this circular letter, all information is without guarantee.

Settlement with the relevant canton

Until now, a company could only settle and deliver withholding taxes in one canton – the canton where its head office is located. This was no longer possible from 1 January 2021. The employer must settle accounts with the relevant canton in each case.

The eligible canton is the canton in which the employee is liable to pay tax. In principle, this is the canton of residence or weekly residence of the employee subject to withholding tax. If the employer is resident abroad and without a weekly place of residence in Switzerland, the canton in which the employer has its registered office, its actual administration or its permanent establishment is entitled to claim.

In order for the withholding tax statements to be transmitted to the cantonal tax authorities via the uniform wage reporting procedure (ELM-QST), the employer must register with the competent tax authority in all relevant cantons and request a customer number. This information must be supplemented in KLARA under Company-> Place of work and opening hours-> Withholding tax information. Importantly, if the data here is missing or incorrect, the withholding tax cannot be transmitted electronically.

Reduction of entitlement provision

The cantons may set the remuneration for the employer's participation at 1 to 2%. It can therefore be assumed that the entitlement provision commission will be reduced in most cantons.

Change from withholding tax to ordinary taxation

Uniform regulation throughout Switzerland for switching to the ordinary tax procedure: if a person subject to withholding tax receives the settlement permit (C permit) or if a person subject to withholding tax marries a person who is in possession of Swiss citizenship or the C permit, he or she is no longer subject to withholding tax from the following month and is properly assessed for the entire year. The withholding taxes already paid are credited interest-free.

Harmonisation of monthly and annual model

Two binding calculation models have been worked out.

Annual model

This applies to the cantons of Vaud, Geneva, Valais, Freiburg and Ticino.

The monthly gross income is decisive for the calculation of the withholding tax deduction. The average income of the whole year is taken into account to determine the percentage (rate-determining salary).

Monthly model

This applies to all other cantons.

When calculating withholding tax according to the monthly model, the month is considered a tax period. For the calculation of the withholding tax deduction, the current gross income is decisive, i.e. all taxable benefits paid out to the employee subject to withholding tax in the corresponding month are usually to be added together and determine the percentage for the current month as a whole.

Tariff classification

A uniform application now applies for all cantons in the absence of tariff classification. If the employee does not reliably prove their personal circumstances, the debtor for the taxable benefit applies the following tariffs:

- For single persons and for employees of indefinite civil status, tariff code A, without children and with church tax (A0Y)

- For married employees, tariff code C, without children and with church tax (C0Y)

Elimination of tariff code D and new tariff code G

Tariff code D is no longer applicable to income from a secondary occupation and to replacement income (daily allowances, partial pensions, benefits of third parties liable for compensation). For replacement income (daily allowances, partial pensions, benefits of third parties liable for compensation) that are not paid out via the employer to the person subject to withholding tax, the tariff code G (or tariff code Q for German cross-border commuters) now applies.

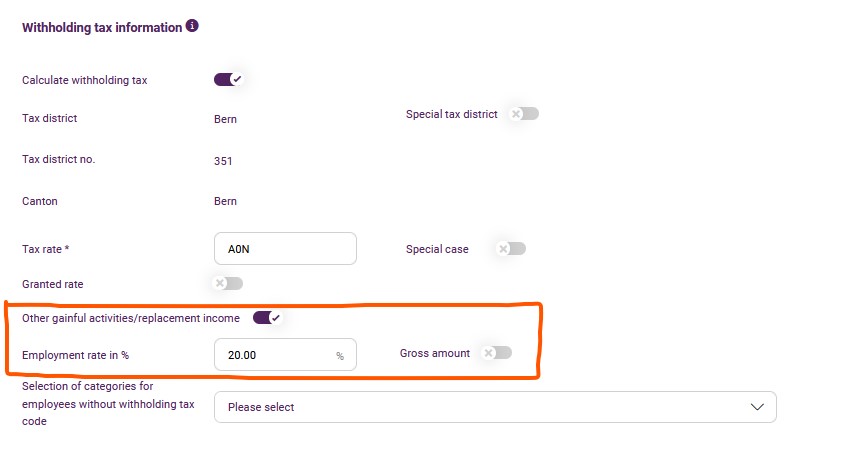

If a person subject to withholding tax pursues several gainful activities at the same time or receives wage payments and/or replacement income from different employers (including outside Switzerland), the rate-determining income for each employment or insurance relationship must be determined as follows:

- Conversion to the effective overall level of employment of all gainful activities (including replacement income) of the employee.

- Conversion to a level of employment of 100 percent if the effective overall level of employment is not disclosed by the employee.

- Conversion to the actual total gross income, provided that the income is known or disclosed to the employer (for example, in the group or several employment contracts with the same employer).

- If the working hours of employment cannot be determined (for example, for a flat-rate part-time caretaker position), the employer can offset the amount used in the relevant tax year for the calculation of tariff code C to determine the rate-determining income.

Example: employees have part-time working hours totalling 80% (gross salary of CHF 8,000) and additionally stated that they have other employment constituting 20%. For the employee, further employment can be recorded under withholding tax data in order to be able to determine the rate-determining income. Instead of the working hours percentage, a gross amount can also be specified.

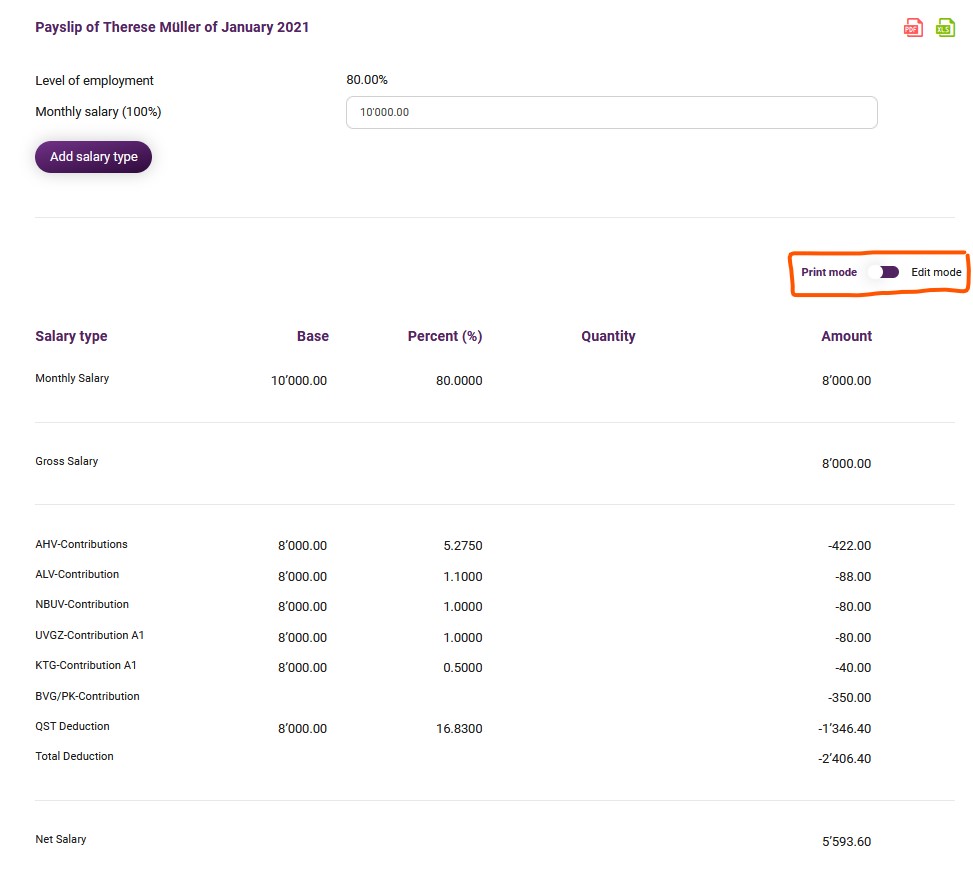

In payroll accounting, this is shown as follows: change print view to input view in order to be able to check the rate-determining income.

In the input view, the rate-determining income is then visible at the very bottom. In our example, this is CHF 10,000 (80% working hours, CHF 8,000 gross + the other employment of 20%, CHF 2,000). This rate-determining income is used to identify the percentage in the tariff table for withholding tax deduction.

Withholding tax basis offsetting

Employee contributions and benefit obligations for the employee assumed by the employer are still subject to withholding tax.

Fortunately, the tax authorities of all cantons have been able to agree that the following employee contributions are not subject to withholding tax if they are adopted equally for all employees or groups of employees defined in the company’s regulations:

- Employer benefits with regard to purely patron-financed pension funds;

- Employer contributions to compulsory accident insurance, occupational accident insurance (OAI) and non-occupational accident insurance (NOAI);

- Contributions for collective daily allowance and collective supplementary insurance (UVG/AI) taken out by the employer.