If you do not debit a purchase in the current expenditure but instead have to enter it on the assets side, it is necessary that you enter this position in the opening balance sheet in KLARA in advance. If you are in the first financial year in KLARA, this will be under accounting in the opening balance sheet. If you have already concluded the first financial year in KLARA, click on “Set up accounting” in the year-end processing in the corresponding year.

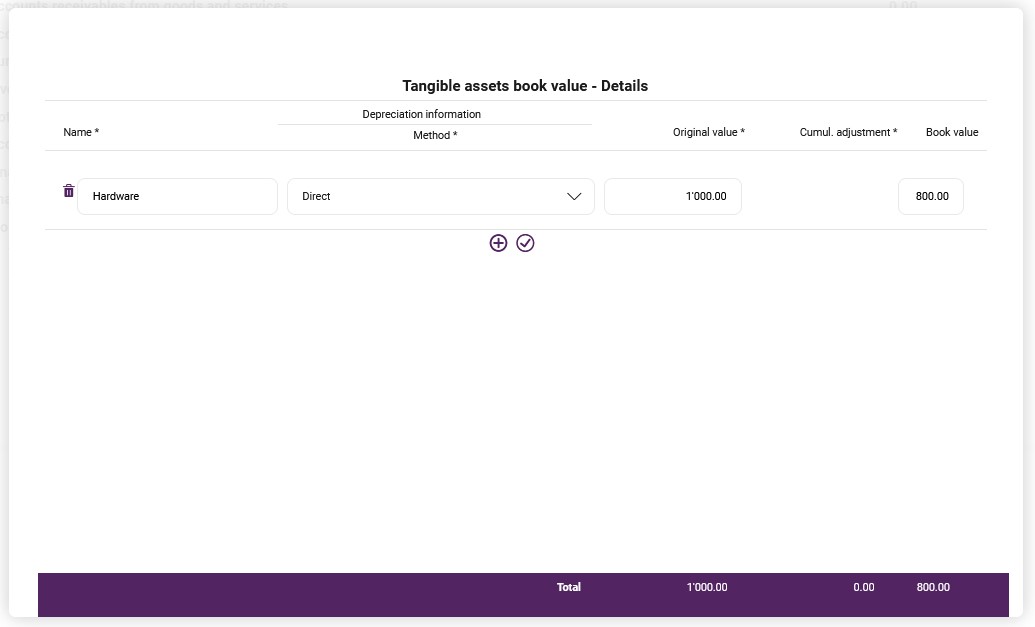

Then open the detail page under the relevant position in the fixed assets and enter the required asset. In addition to the name for the position also the depreciation method. If you are in your first year in KLARA and have stated that your company is older than this, you will also be requested to enter the original value and the book value. You will find this information in the accounts closing for the previous year. If you are no longer in the first year in KLARA and you have procured a new asset, you can no longer enter a procurement or book value. In this case the position must be opened analogously, but the values must be posted via a posting, e.g., via the business case “Investment expenditure fixed assets” in the automatic posting procedure.

Method: The way in which the depreciation must be posted.

Direct:

The depreciation is deducted directly from the position, i.e. in the first year procurement value 1000 – depreciation 200 gives a new book value on the account of 800.

Indirect:

The depreciation is not posted from the same account but from a separate write-down position. For example, until it is sold or scrapped the asset remains at the original procurement cost of 1000. At the same time the write-down account increases every year by the depreciation (balance in the balance sheet increases in negative value): 1st year -200, 2nd year -400, etc.

Please note that KLARA does not calculate any automatic depreciation. However, this information will help you to calculate the depreciation within the framework of the annual closing. Depreciation can be carried out in KLARA in the manual posting screen (manual type or general ledger).

Important: Please be sure to observe the laws, provisions and customary practices of your cantonal tax administration as well as those of the Federal Tax Administration. In addition, the corresponding provisions of the Code of Obligations must be complied with. Also, it is not necessary for every minor amount (e.g. computer mouse) to be capitalised, the delineation of what must be capitalised and what has to be debited to expenses is dependent on the specific situation of your company. Your fiduciary can advise you regarding permissible capitalisation and depreciation procedures.