The private account serves to keep the business and private realms clearly separate. In business accounting, no private expenses may be deducted from the business profit. In the simplest terms, this separation works in that distinct bank accounts are used in each case and any private purchases, etc. are made separately.

If a mix of private and business matters cannot be avoided, private purchases can be posted to the “private account” in the accounting.

Technically, the private account works as follows:

- Positive balance (postings in CREDIT): business expenses were paid with private funds.

- Negative balance (postings in DEBIT): business funds were used privately.

At the beginning of each new financial year, the balance of the private account is offset against capital. In KLARA, this can be done with a manual posting.

In KLARA, the following accounts are available for the posting of private transactions:

- Cash purchases: this account can be used for private purchases as well as private deposits. In principle, all private transactions can be processed via this account. The following accounts can be used for a more detailed breakdown, but this is not mandatory.

- Payment in kind

- Private elements of operating expenses

- Private apartment rental value

- Private insurance premiums

- Private pension contributions

- Private taxes

- Other

Two examples of the two most frequent postings in the private account:

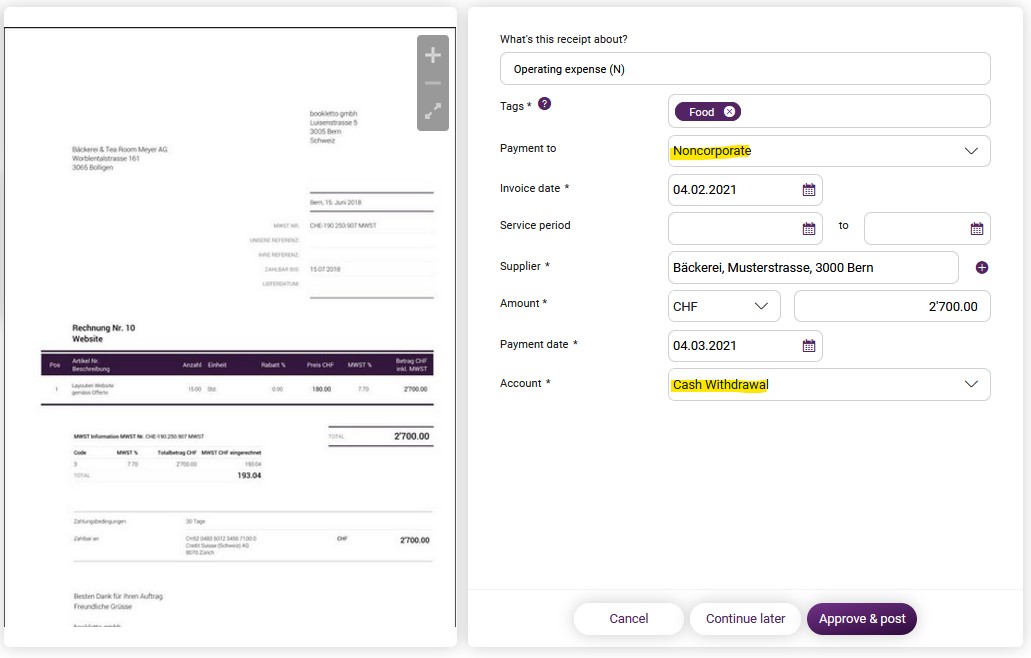

1. You have just become self-employed and have not yet opened a new bank account for your company. You paid the first invoices for the newly founded sole trader company using your private bank account or cash. So that you can still post the expenses, which were for business purposes, you select the payment method “Private” when posting in the booking workflow.

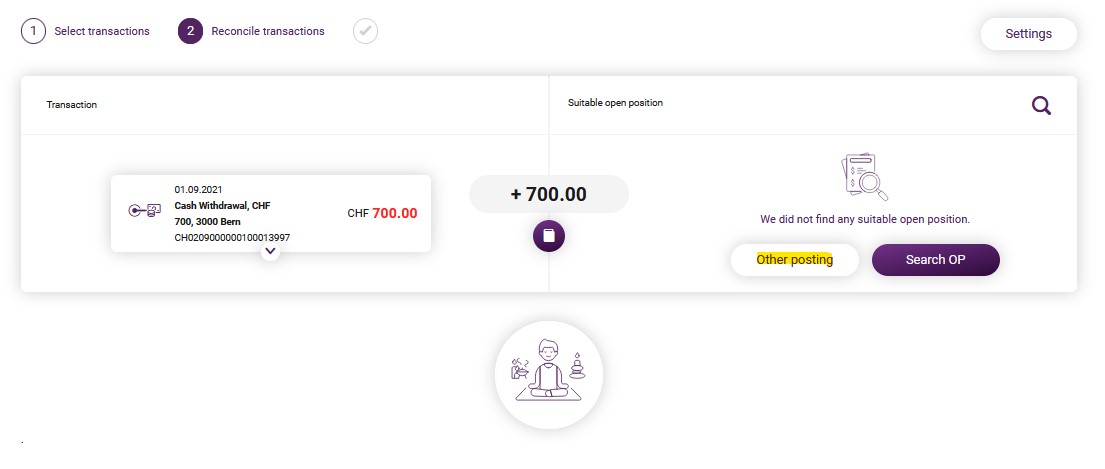

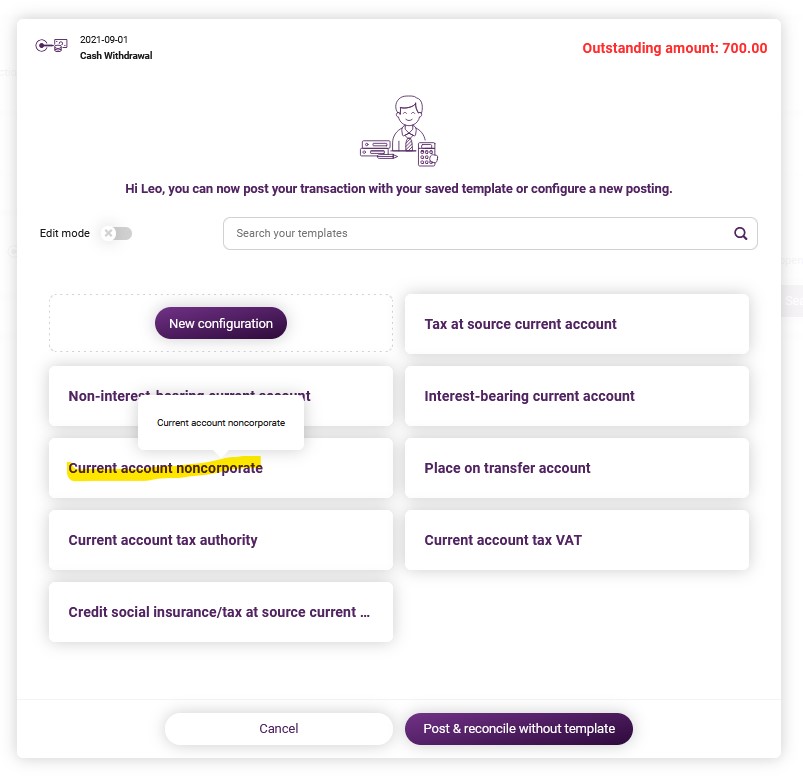

2. You have withdrawn cash from the business account at the ATM, which you will use for private purposes. Do the business accounting and book the private reference with the following option: click on the book icon, select “Other”, then select “Private account”.

If you are the owner of a limited company or joint stock company, and you do not have a private account, you can set up a non-interest-bearing current account which works in the same way.